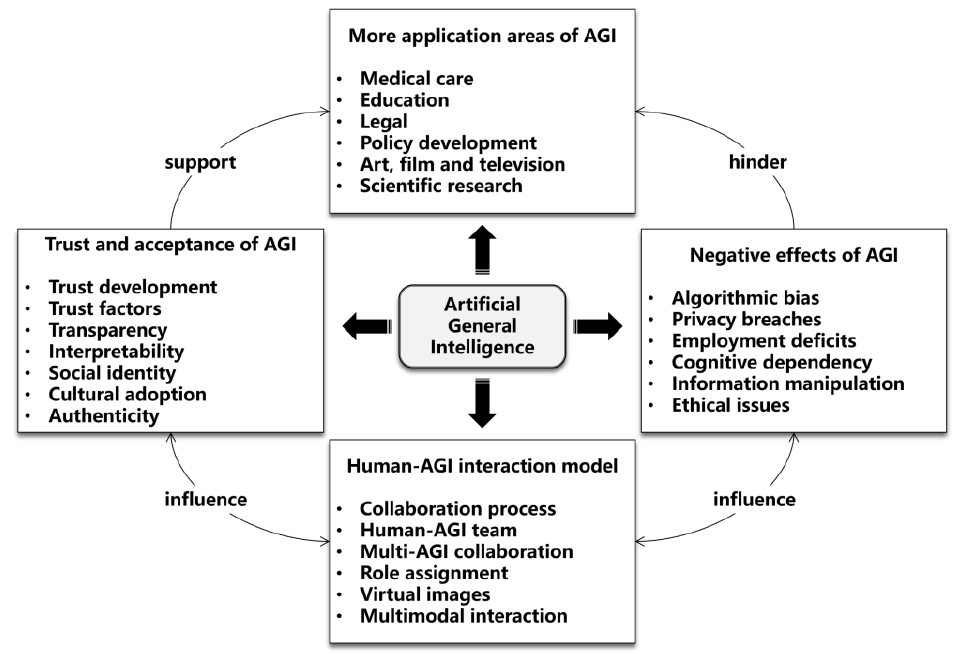

Artificial General Intelligence (AGI) can understand, learn, and apply knowledge across a range of tasks, in a similar way to humans. It is not limited to specific tasks. In e-commerce, AGI is revolutionizing the industry by enabling highly personalized shopping experiences, intelligent customer service, and efficient supply chain management. However, it also raises concerns about job losses and invasion of privacy (Cheng et al. 2025). Autonomous decision-making also has ethical implications.

Figure 1. Future trends in AGI research

In supply chain and operations management, AGI-driven tools like Deepseek can forecast demand better than before, coordinate logistics, and solve problems independently in real time. When organizations learn how to use these tools, they can adopt them faster and improve the overall supply chain performance. Alibaba’s smart warehouse demonstrates how AGI uses data, algorithms, and robots to automate inventory management, reduce errors, and enhance labour productivity through the collaboration between AI and human expertise. In marketing, AGI enables highly personalized strategies by creating content that resonates emotionally with customers. AI-generated virtual influencers with emotional expressions, such as happiness or surprise, can significantly increase user engagement, especially when combined with visually appealing content. AGI also excels at creating ads with agentic appeals, like messages focusing on efficiency. Consumers prefer these ads because they enhance the sense of self-efficacy in completing tasks. However, for ads that require emotional storytelling, human-AI collaboration remains crucial. Generative AI can also deliver highly personalized marketing content, outperforming traditional digital tools in terms of relevance and efficiency. In customer service, AGI-powered digital assistants build trust and encourage purchase intent by using anthropomorphic features. Computers become social actors. By improving response speed and problem-solving accuracy, AI chatbots can improve customer satisfaction and loyalty. Their effectiveness depends on balancing technical capabilities with human-like interactions. In industries such as hospitality and tourism, AGI tools like Deepseek can personalize recommendations and simplify backend operations, showing their adaptability across different sectors. A bibliometric review indicates that e-commerce AI research has long focused on recommendation systems, sentiment analysis, and personalization. Now, AGI is expected to integrate these areas into a cohesive, autonomous ecosystem. Collaborative AI frameworks emphasize combining AGI’s mechanical and thinking intelligence with human marketers’ intelligence. This allows humans to focus on strategic and emotional tasks while AGI automates routine processes.

Reference Cheng, X., Mou, J., Wang, Y., & Zarifis, A. (2025) ‘Development of AGI in e-commerce’, Journal of Electronic Commerce Research, vol.26, no.3, pp.163-169. http://www.jecr.org/node/737

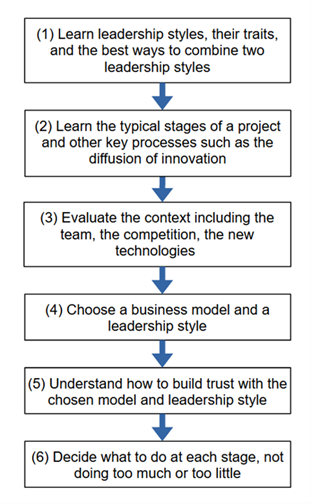

When we think of great leaders, we turn to famous leaders from history for inspiration, but they did not have to deal with unpredictable disruption AI is causing. The modern leader must not only lead humans, but also autonomous AI agents. They must also guide the organization through the process of adapting to fully utilize AI across all the operations. There is no simple answer to this challenge, but there is a structured approach with six steps that will increase the chances of success.

Figure 1. The steps to being a great leader in the age of AI

Step 1: Learn the three most effective leadership styles

The first step is to learn the three most effective leadership styles and understand the benefits of combining them in various ways. These are servant, transactional and transformational.

Step 2: Learn the typical stages of a project

The modern leader must constantly integrate the latest versions of AI so their role becomes similar to that of a project manager implementing a series of digital transformation projects. Typically, a project has six stages that are forming, storming, norming, performing, adjourning and post-project collaboration.

Step 3: Evaluate the context

While we are fascinated by the capabilities of AI, the role of the context the leader finds themselves in must not be underestimated. The leadership approach must consider the influence of the context on the people and the technology.

Step 4: Choose a business model and a leadership style

The leader needs to think about whether to focus on one of the three leadership styles or combine two of them to get the best out of the situation they are in.

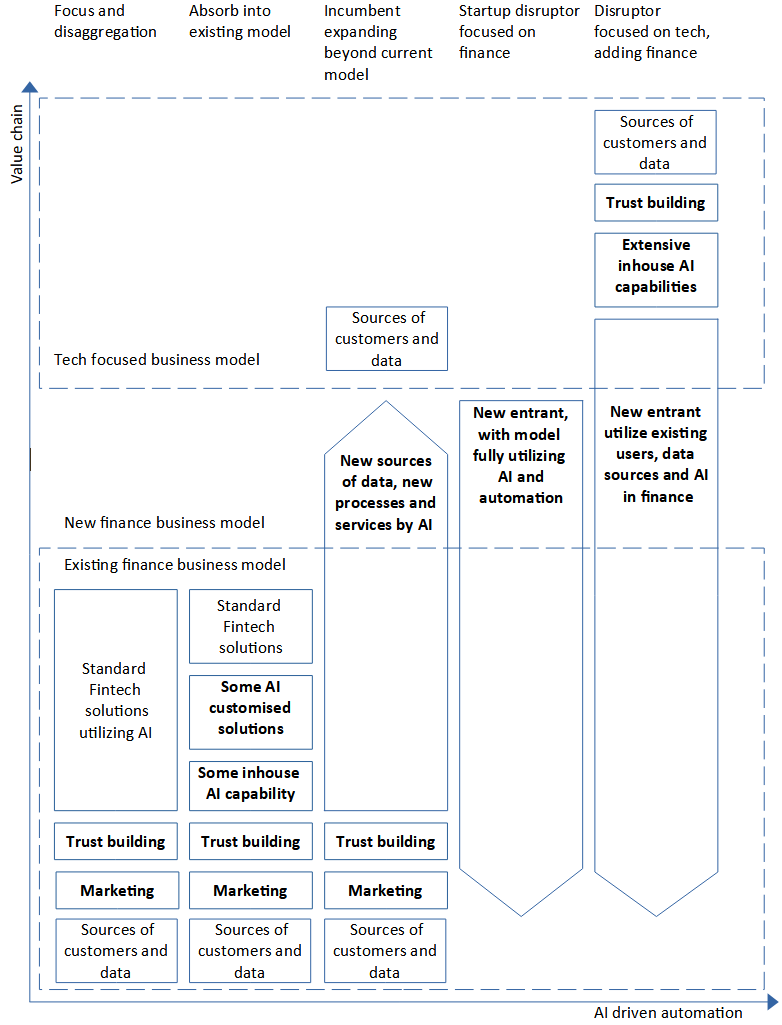

Choosing a proven AI centred business model will offer clarity. There are six proven AI focused business models: first: incumbent focusing on one part of the value chain and disaggregating, second: incumbent absorbing AI into existing model, third: incumbent expanding beyond current model to fully utilise the opportunities of AI and access new data, fourth: startup disruptor focused on one sector, built from the start to be highly automated, fifth: disruptor focused on tech adding a new service such as insurance, and lastly the sixth model is a disruptor that is not tech-focused but has an extensive userbase.

Step 5: Build trust with a clear vision of what the role of AI is

To lead autonomous AI agents, the leader must build trust in them among the team. The leader must be clear on their use and build a consensus around this. The team must be put on a sustainable trajectory for change.

Step 6: Decide what to do at each stage of the project

Effective leadership today must involve leading on technology as well as people, building trust in the technology, and finding the best combination of leadership styles to get the most out of humans and automated AI agents. These many tasks cannot all be done at once so the leader must have a plan of what they will focus on at each stage.

The steps touched on here are covered more thoroughly in the book. If you want to learn more about Leadership in AI with trust you can buy my book from all good bookshops.

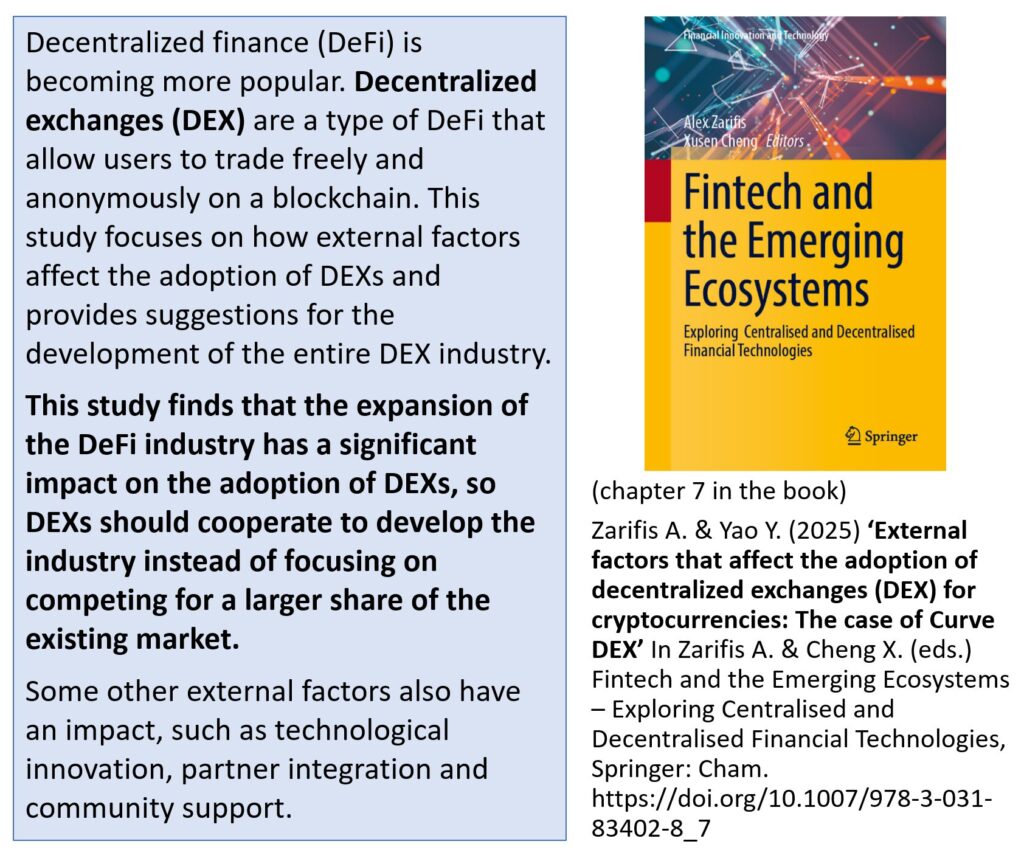

Decentralized finance (DeFi) is becoming more and more popular. Decentralized exchanges (DEX) are a type of DeFi that allow users to trade freely and anonymously on a blockchain. There are two platforms for cryptocurrency trading, centralized exchange (CEX) and DEX. Most of the exchange volume is happening at CEX because they are easier to use. However, DEXs volume is catching up. The reasons for the popularity of DEXs are linked to the unique advantages of DeFi. First, CEX is a business that requires Know Your Customer (KYC). It requires customers’ identification for registration to comply with anti-money laundering regulations and any other laws from the countries its customers come from. Because of this, users are still concerned about several issues such as privacy and the risk of their wealth being confiscated. This study focuses on how external factors affect the adoption of DEXs and provides suggestions for the development of the entire DEX industry. The study finds that the expansion of the DeFi industry has a significant impact on the adoption of DEXs, so DEXs should cooperate to develop the industry instead of focusing on competing for a larger share of the existing market. Some other external factors also have an impact, such as technological innovation, partner integration and community support. As DeFi is closely related to the adoption of DEX, the study also discusses the external factors that may affect the adoption of DeFi, namely trust, infrastructure, and regulation.

Figure 1. The factors that affect the adoption of Decentralised Exchanges DEX

Related research is mainly focused on the difference between DEXs, and tries to find how a DEX can gain an advantage over other DEXs, but this research concentrates on the external factors to show how to encourage DEX adoption. While market fluctuations may attract short-term attention and reactions, the long-term development of DEX relies on a stable user base in DeFi and continued expansion of the industry. This research enriches the theoretical framework of DeFi and sheds light on the relationship between DeFi and DEX. A DEX relies on the liquidity of DeFi, with higher liquidity on the blockchain, the DEX liquidity is expected to be higher, leading to slippage, which means the loss that users suffer when trading on DEX, is reduced. This research provides new insights into understanding the liquidity dynamics of DEXs, extending existing theory on the interplay between liquidity and transaction costs.

References Zarifis A. & Yao Y. (2025) ‘External factors that affect the adoption of decentralized exchanges (DEX) for cryptocurrencies: The case of Curve DEX’ In Zarifis A. & Cheng X. (eds.) Fintech and the Emerging Ecosystems – Exploring Centralised and Decentralised Financial Technologies, Springer: Cham. https://doi.org/10.1007/978-3-031-83402-8_7

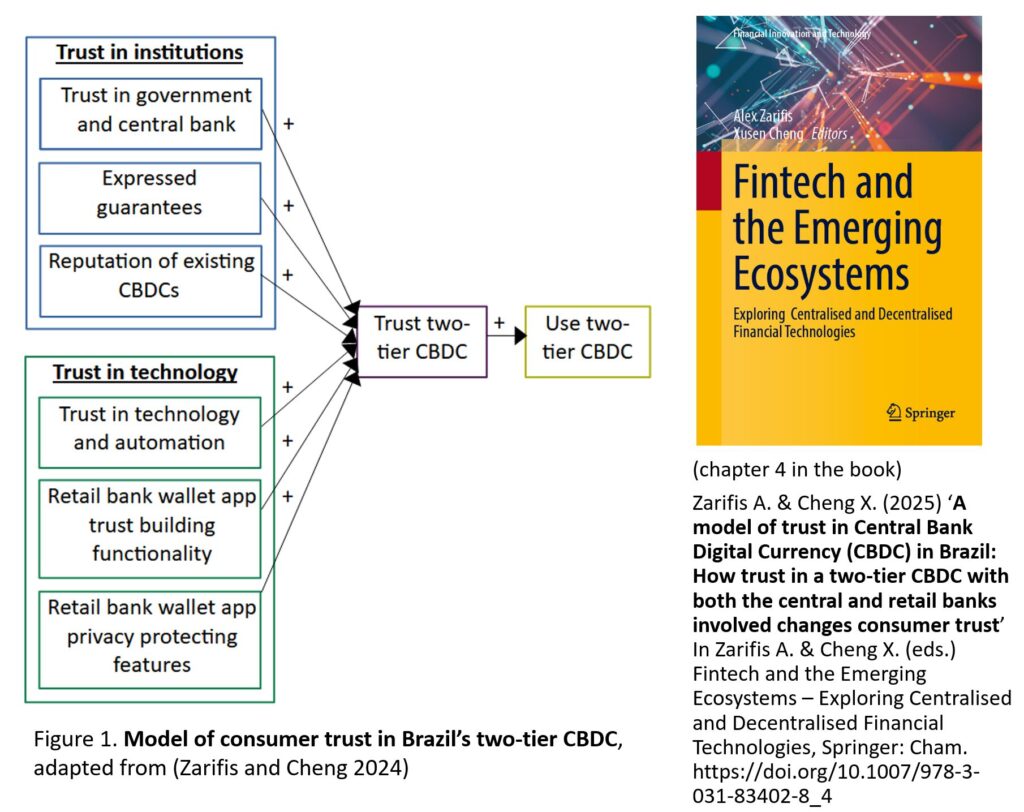

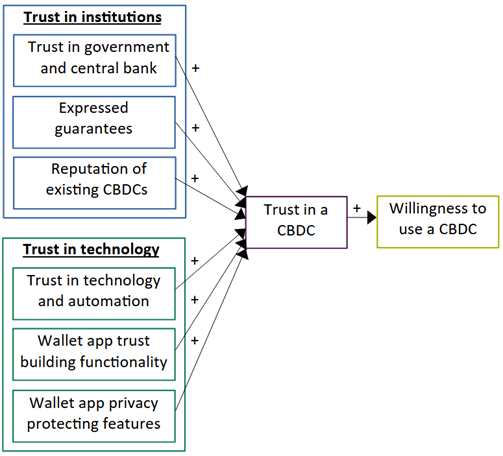

(chapter 4 in book) Central bank digital currencies (CBDC) have been implemented by some countries and trialled by many more. As the name suggests, the fundamental characteristics are that this is money that is digital, without a physical note or coin, and issued by a central bank. The consumer has an increasing range of financial services to choose from including decentralised blockchain based cryptocurrencies. A CBDC may use blockchain technology, but it is centralized, so the institutions that support it play an important role. While being centralised may reduce some risks, it may inadvertently increase others. Despite the centralised top-down nature of this financial technology, it still needs to be adopted so the consumer’s perspective, particularly their trust in it, is very important. Each CBDC implementation can be different, and each country’s context can be different, therefore it is important to understand each case separately. This research models the Brazilian consumer’s trust in their two-tier CBDC, where the central bank and the retail banks retain their current role (Zarifis and Cheng, 2025). This implementation is not a one tier solution where retail banks are bypassed in some ways, and the citizen interacts mostly with the central bank. Existing research that identified six ways to build trust in a different CBDC (Zarifis and Cheng, 2024) was used as a basis. This research tested a model with one additional way to build trust, but this additional way to build trust was not supported. The seventh hypothesized way that is not supported is that the implementation process, including pilot implementations, would build trust. Therefore, despite the differences in the Brazilian CBDC, the original model applies here also which suggests the model applies for both two-tier solutions, and mixed one and two-tier solutions.

Figure 1. Model of consumer trust in Brazil’s two-tier CBDC, adapted from (Zarifis and Cheng 2024)

Three institutional, and three technological factors, are found to play a role. The six ways to build trust that are supported are: (a) Trust in government and central bank offering the CBDC, (b) expressed guarantees for those using it, (c) the favourable reputation of other active CBDCs, (d) the CBDC technology, the automation and limited human involvement necessary, (e) the trust building features of the CBDC wallet app, and (f) the privacy features of the CBDC wallet app and back-end processes. It is important to develop user centered services in Brazil so that trust is built in the services themselves, and the government institutions that deliver them, sufficiently for broad adoption.

References Zarifis A. & Cheng X. (2024) ‘The six ways to build trust and reduce privacy concern in a Central Bank Digital Currency (CBDC)’. In Zarifis A., Ktoridou D., Efthymiou L. & Cheng X. (ed.) Business digital transformation: Selected cases from industry leaders, London: Palgrave Macmillan, pp.115-138. https://doi.org/10.1007/978-3-031-33665-2_6 (open access)

Zarifis A. & Cheng X. (2025) ‘A model of trust in Central Bank Digital Currency (CBDC) in Brazil: How trust in a two-tier CBDC with both the central and retail banks involved changes consumer trust’ In Zarifis A. & Cheng X. (eds.) Fintech and the Emerging Ecosystems – Exploring Centralised and Decentralised Financial Technologies, Springer: Cham. https://doi.org/10.1007/978-3-031-83402-8_4 (open access)

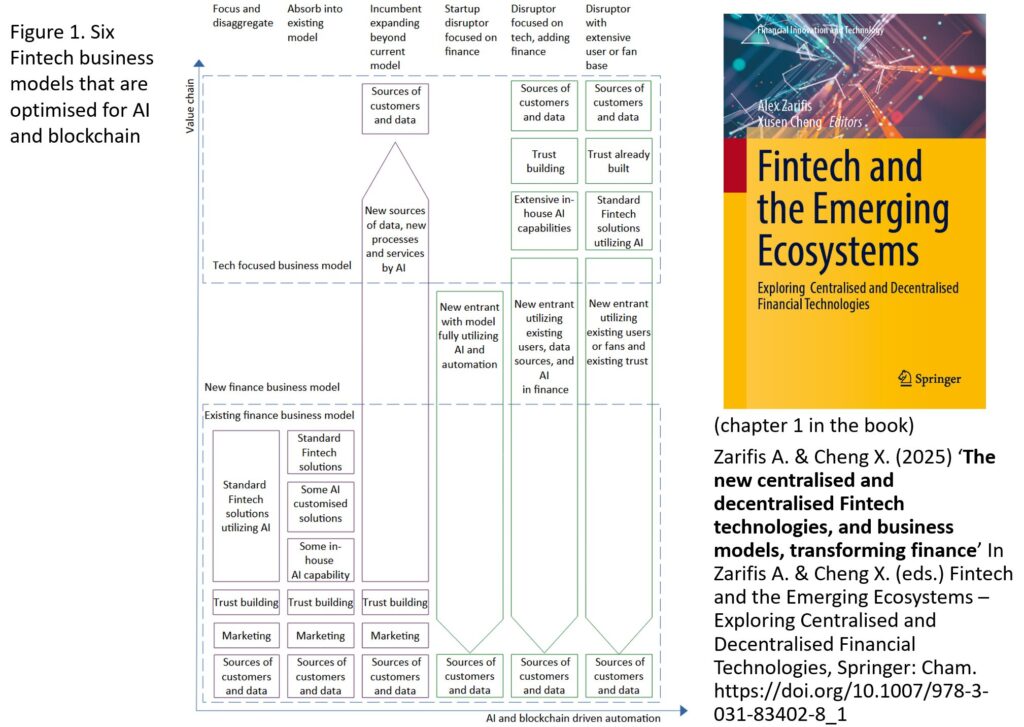

Different organizations see this period of transition and adjustment as either an opportunity or a threat. Some from outside the financial sector such as bigtech see it as an opportunity to take market share. Others have managed to limit competition and have regulatory ‘moats’ around the financial services they provide, that they would prefer to maintain. Whether an existing financial organization decides to keep their existing model, disrupt themselves in a drastic way, or evolve gradually into a new business model, it is important that they understand this multifaceted transformation. While startups are like agile speedboats that can change direction easily, large financial organizations more closely resemble large cruise ships that need to know where they will be in five years’ time, before setting a course to get there.

This research finds support for six Fintech business models that are optimised for AI and blockchain. These are (1) focus on less financial services and disaggregate, (2) absorb AI into existing financial model, (3) incumbent in finance expanding beyond current model, (4) new dedicated startup in finance disrupting the established ways of operating, (5) tech company disrupting finance, (6) disruptor not focused on technology with extensive user-base. The first three models involve organizations that are already active in the finance sector. The last three models are new organizations using AI to start offering financial services.

While the sixth model has similarities to the fifth, it also has some distinct features. The key characteristics are that it has an existing user base, with which trust has already been built, and unlike the fifth model, it uses advanced but commoditised financial technology. Despite the ongoing innovation, some Fintech transitioning into a commoditised service, that is easily deployed, is a sign of a maturing sector.

Figure 1. Six Fintech business models that are optimised for AI and blockchain

It is important to appreciate that existing trust with customers or fans, or the ability to build trust, are important parts of the value chain. Having the capability to build trust can be the starting point, with financial services added to it. Is the technology still the most critical factor in a Fintech at this stage, or the ability to build trust in it? Words such as modularity and ecosystem are often used, but it is important to understand how a new Fintech can be created, its journey and how it can build momentum and carve out a niche with technology and trust.

Reference: Zarifis A. & Cheng X. (2025) ‘The new centralised and decentralised Fintech technologies, and business models, transforming finance’ In Zarifis A. & Cheng X. (eds.) Fintech and the Emerging Ecosystems – Exploring Centralised and Decentralised Financial Technologies, Springer: Cham. https://doi.org/10.1007/978-3-031-83402-8_1

By Dr Alex Zarifis, originally published in The Conversation

I have a confession to make. Despite being an academic, I do not actually read many books. In truth, I don’t often find books about what I like. My interest is on how the latest technologies affect business, and this topic is usually covered better by research articles and the press.

In the days when I was a student and money was tight, I was even less likely to buy books. But one exception was Wikinomics: How Mass Collaboration Changes Everything (2006). Written by Canadian tech thinkers Dan Tapscott and Anthony D. Williams, it captured my interest in how new innovations can change our personal and professional lives – and how exciting this change can be. Clearly I was by no means the only one that felt this way, as the book became a tremendous success.

The title, a compound of Wikipedia pages and economics, followed in the style of the equally successful Freakonomics (2005), but Wikinomics is very much a landmark in its own right. What it conveyed powerfully was that the level of mass collaboration and sharing online was about to move way beyond what we had seen in the first 15 years of the internet, transforming how people did business.

These were much more than mere technological advances, the book argued, and would require a completely different business mindset and philosophy. This was all about openness, sharing, freedom to innovate, and acting globally.

Wikinomics highlights seven new models of collaboration:

1. Open-source software: Software whose source code is made available for everyone to use and build on, which provides a way for firms and coders to coalesce around the same standard. One of the key early driving forces was the Linux operating system, while the book also points to Wikipedia as the archetypal example of the collaborative mindset.

Today, we see many examples of standalone coders coming together from around the world to build applications that are decentralised, meaning they’re not owned by anyone or based anywhere. Decentralised finance (defi), for instance, is offering a new way for people to do everything from trading financial assets to taking out mortgages.

2. Crowdsourcing innovative talent: This allows organisations to solve problems with ideas from outside, typically from other parts of the world. The example given in the book is InnoCentive (now Wazoku Crowd), a site where organisations post scientific challenges and offer rewards for their solution.

3. Prosumers: These are forward-thinking consumers who co-create products and services. In 2006, for instance, users of the virtual world, Second Life, were creating virtual buildings then renting them to other users. Today, fans of computer games such as Total War: Warhammer III are creating new characters and environments in a similar way.

4. Innovators sharing information: Making data widely available for others to use has particular importance in helping solve humanity’s greatest challenges, such as climate change. The increasing popularity of open-access publishing of academic research has been an important step in this direction.

5. Open platforms: Software that allows largely unrestricted access to its content and data gives businesses and individuals more room to collaborate and create new products. One example in the book is Google Maps, which was used by US entrepreneur Paul Rademacher to create a service called HousingMaps. It took data from Craigslist about homes for sale in a given area and pinned them on a map so that anyone searching for a home could see all the available locations at the same time.

Combining capabilities in this way became known as mash-ups, and can be seen today in a service like online bank Revolut. Revolut brings together services and information from a broad variety of organisations and offers them in an integrated way that is easy to use.

6. Mass collaboration in manufacturing: The book noted how a manufacturer like Boeing had shifted from designing everything in-house and sourcing specified parts from individual suppliers to instead having suppliers working together to design parts themselves and then assemble them in teams in Boeing factories.

This switch in emphasis from supply chains to ecosystems has more recently been typified by Shenzhen in China, where collaborative manufacturing in everything from circuits to touchscreens blurs the boundaries between the companies involved.

7. Modern workplaces that avoid hierarchies and silos: Instead of rigid structures, the driving force is social connectivity and fun.

Pros and cons

As is often the case with hugely successful books, Wikinomics was a combination of a great title, good writing and timing. By 2006 many of these trends were well underway. For instance, it was already common for coders to use open-source software like Linux for mass global collaboration. But if the book had been more original, it would not have been so well timed for mass market appeal.

A common criticism of Wikinomics is that it created many obscure terms that will only be familiar to those who have read the book. For example, its fourth collaborative model is called “ideagoras”, which hasn’t exactly caught on. No doubt the authors could have used simpler existing terms, but this is not the main weakness of the book.

With the benefit of hindsight, Wikinomics emphasised the positives of mass collaboration but did a poor job of foreseeing the challenges. Openness has made the world much more vulnerable to cybersecurity hacks, frauds and privacy breaches. Our behaviour online is now endlessly recorded and analysed, making people feel both distrustful and powerless.

What the book did do very well was to frame the issues around the new collaborative economy and explain them clearly. It helped readers to organise the new and old information in their minds, making it easier for them to analyse developments and be part of the revolution.

As a lecturer that teaches business on an executive MBA course to experienced managers, this is something I can appreciate. I cannot always tell them something they have not heard before, but if I can frame the issues well and communicate them clearly, it’s still useful to them. This is ultimately what Wikinomics did: it helped clarify the issues readers already had some understanding of, helping to shape the business zeitgeist for web 2.0.

Central Bank Digital Currencies (CBDC) are digital money issued, and backed, by a central bank. Consumer trust can encourage or discourage the adoption of this currency, which is also a payment system and a technology. CBDCs are an important part of the new Fintech solutions disrupting finance, but also more generally society. This research attempts to understand consumer trust in CBDCs so that the development and adoption stages are more effective, and satisfying, for all the stakeholders. This research verified the importance of trust in CBDC adoption, and developed a model of how trust in a CBDC is built (Zarifis & Cheng 2023).

Figure 1. Model of how trust in a Central Bank Digital Currencies (CBDC) is built in six ways

There are six ways to build trust in CBDCs. These are: (1) Trust in government and central bank issuing the CBDC, (2) expressed guarantees for the user, (3) the positive reputation of existing CBDCs active elsewhere, (4) the automation and reduced human involvement achieved by a CBDC technology, (5) the trust building functionality of a CBDC wallet app, and (6) privacy features of the CBDC wallet app and back-end processes such as anonymity. The first three trust building methods relate to trust in the institutions involved, while the final three relate to trust in the technology used. Trust in the technology is like the walls of a new building and institutional trust is like the buttresses that support it.

This research has practical implications for the various stakeholders involved in implementing and operating a CBDC but also the stakeholders in the ecosystem using CBDCs. The stakeholders involved in delivering and operating CBDCs such as governments, central banks, regulators, retail banks and technology providers can apply the six trust building approaches so that the consumer trusts a CBDC and adopts it.

Dr Alex Zarifis

Reference

Zarifis A. & Cheng X. (2023) ‘The six ways to build trust and reduce privacy concern in a Central Bank Digital Currency (CBDC)’. In Zarifis A., Ktoridou D., Efthymiou L. & Cheng X. (ed.) Business digital transformation: Selected cases from industry leaders, London: Palgrave Macmillan, pp.115-138. https://doi.org/10.1007/978-3-031-33665-2_6

Fintech is changing the services to consumers, and their relationship with the organizations that offer them. This change is neither top-down nor bottom-up, but is being driven by many different stakeholders in many different parts of the world, making it hard to predict its final form. This research identifies five business models of Fintech that are ideal for AI adoption, growth and building trust (Zarifis & Cheng, 2023).

The five models of Fintech are (a) an existing financial organization disaggregating and focusing on one part of the supply chain, (b) an existing financial organization utilizing AI in the current processes without changing the business model, (c) an existing financial organization, an incumbent, extending their model to utilize AI and access new customers and data, (d) a startup finance disruptor only getting involved in finance, and finally (e) a tech company disruptor adding finance to their portfolio of services.

Figure 1. The five Fintech business models that are optimised for AI

The five Fintech business models give an organization five proven routes to AI adoption and growth. Trust is not always built at the same point in the value chain, or by the same type of organization. The trust building should usually happen where the customers are attracted and on-boarded. This means that while a traditional financial organization must build trust in their financial services, a tech focused organization builds trust when the customers are attracted to other services.

This research also finds support that for all Fintech models the way trust is built, should be part of the business model. Trust is often not covered at the level of the business model and left to operation managers to handle, but for the complex ad-hoc relationships in Fintech ecosystems this should be resolved before Fintech companies start trying to interlink their processes.

Alex Zarifis

Reference

Zarifis A. & Cheng X. (2023) ‘The five emerging business models of Fintech for AI adoption, growth and building trust’. In Zarifis A., Ktoridou D., Efthymiou L. & Cheng X. (ed.) Business digital transformation: Selected cases from industry leaders, London: Palgrave Macmillan, pp.73-97. https://doi.org/10.1007/978-3-031-33665-2_4

Digital transformation is being driven by AI that is acting as a catalyst for business advancement. We looked at eight cases of digital transformation and found nine key themes. We looked at cases of digital transformation in finance, tourism, transport, entertainment and social innovation (Zarifis et al. 2023).

Figure 1. The tightly coiled ‘spring’ of digital transformation leader’s innovation, and the followers

The first of the nine main themes identified here is: (1) Digital transformation leaders will constantly innovate, while digital transformation laggards will have a stop-start approach. Digital transformation leaders will rapidly innovate going through regular iterative evolutions of their technologies, moving through repeated cycles of agile developments metaphorically forming a ‘spring’. New innovations and in-house skills are built up in this process of constant innovation. Continuing with the metaphor this tightly coiled ‘spring’ will store ‘energy’ propelling the organization forward. Digital transformation laggards will have a stop-start approach copying certain solutions of the leaders but not keeping up. Metaphorically a far less tightly coiled ‘spring’.

The other eight themes identified are: (2) There are no simple answers, or a single way to go forward, with digital transformation. (3) Each sector of the economy has its own opportunities, challenges and must find its own path forward. (4) Changes in one sector of the economy, such as the financial sector, will send a ripple of change across other sectors of the economy. (5) Change needs a shared vision, and digital transformation needs leaders to create the shared vision. (6) Digital transformation needs trust and cooperation on every level: Teams, organizations, governments and super-organizations like the EU. (7) People will still have a role: Staff, customers and other stakeholders are still important. (8) There is a dark side of digital transformation that may have not been fully revealed to us yet. (9) Digital transformation should happen hand in hand with sustainability and resilience.

Those are the nine main themes of digital transformation identified based on the cases we looked at. A leader of digital transformation must disassemble the technology, processes, business models and strategies, involved and then put together their own collage of what they want to achieve, and their own montage of the journey there.

Dr Alex Zarifis

Reference

Zarifis A., Efthymiou L. & Cheng X. (2023) ‘Sustainable digital transformation in finance, tourism, transport, entertainment and social innovation’. In Zarifis A., Ktoridou D., Efthymiou L. & Cheng X. (ed.) Business digital transformation: Selected cases from industry leaders, London: Palgrave Macmillan, pp.1-16. https://doi.org/10.1007/978-3-031-33665-2_1

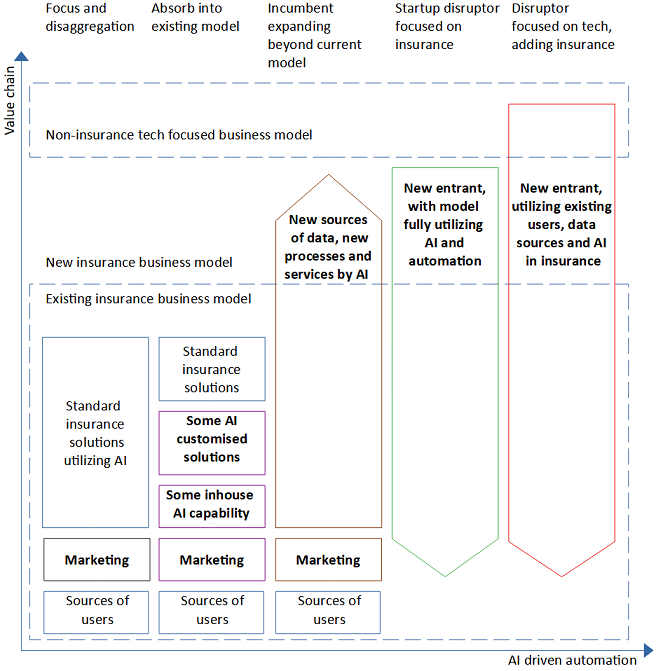

Artificial intelligence (AI) and related technologies are creating new opportunities and challenges for organizations across the insurance value chain. Incumbents are adopting AI-driven automation at different speeds, and new entrants are attempting to use AI to gain an advantage over the incumbents. This research explored four case studies of insurers’ digital transformation. The findings suggest that a technology focused perspective on insurance business models is necessary and that the transformation is at a stage where we can identify the prevailing approaches. The findings identify the prevailing five insurance business models that utilize AI for growth: (1) focus on a smaller part of the value chain and disaggregate, (2) absorb AI into the existing model without changing it, (3) incumbent expanding beyond existing model, (4) dedicated insurance disruptor, and (5) tech company disruptor adding insurance services to their existing portfolio of services (Zarifis & Cheng 2022).

Figure 1. Updated model of five business models in insurance with disruptors split into two types

In addition to the five business models illustrated in Figure 1, this research identified two useful avenues for further exploration: Firstly, many insurers combined the two first business models. For some products, often the simpler ones, such as car insurance, they focused and disaggregated. For other parts of their organization, they did not change their model, but they absorbed AI into their existing model. Secondly, new entrants can be separated into two distinct subgroups: (4) disruptor focused on insurance and (5) disruptor focused on tech but adding insurance.

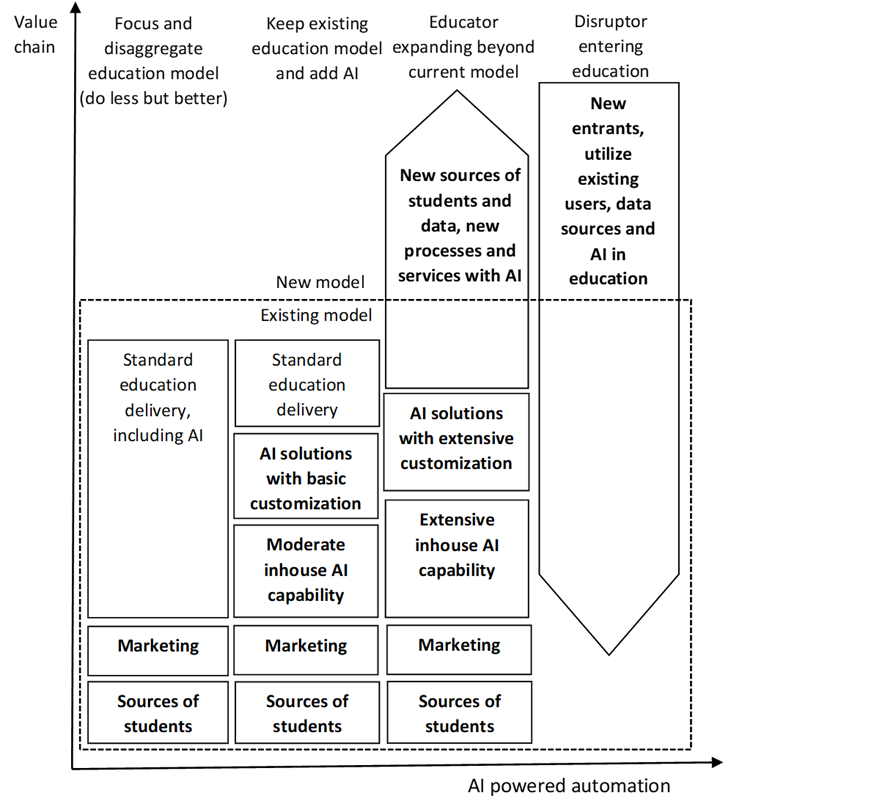

Universities, like many other organizations, are going through a disruptive digital transformation. The alure of AI and automation, allowing smarter, more responsive and scalable universities is clear. What is less clear is what a university will look like five years into this process. We identified four business models that can give leaders a destination for the digital transformation journey (Zarifis and Efthymiou 2022):

(1) This first education business models that is optimized for AI is to focus and disaggregate: In addition to the classroom the successful delivery of education requires a supply chain. With the changes in this supply chain caused by AI an educator can chose to focus on one part of this supply chain. They can focus on the part of the supply chain where their skills are best suited and build an ecosystem for the rest.

Figure 1. Four education business models that are optimised for AI (adapted from (Zarifis, Holland, and Milne 2019))

(2) The second model that is optimized for AI is to keep the existing education model and add AI: Despite the transformational nature of AI, some universities use AI to make the existing model more effective without changing it fundamentally. This may involve more back-office AI applications and less student facing applications.

(3) The third education model that is optimized for AI is an educator expanding beyond the current model: In this model the educator takes advantage of new opportunities emerging from AI and digital transformation. The educator keeps their existing part of the education supply chain, but they also add new processes that take advantage of AI to reach more students and more data.

(4) The fourth model that is optimized for AI is the model of a disruptor entering education: As technology plays a more decisive role in many areas, including education, tech savvy companies can use their advanced systems and existing user base and add other new services. Education can be added as a new feature to a platform in a similar way that banking and insurance services have been added.

The four models presented give a strategic direction and make it easier for the leader of the digital transformation to communicate it. The leader of digital transformation will have to make many choices along this journey, so it is important that all the decisions are compatible with the chosen education business model.

References

Zarifis A. & Efthymiou L. (2022) ‘The four business models for AI adoption in education: Giving leaders a destination for the digital transformation journey’, IEEE Global Engineering Education Conference (EDUCON), pp.1866-1870. https://doi.org/10.1109/EDUCON52537.2022.9766687

Zarifis A., Holland C.P. & Milne A. (2019) ‘Evaluating the impact of AI on insurance: The four emerging AI and data driven business models’, Emerald Open Research, pp.1-17. https://emeraldopenresearch.com/articles/1-15/ (open access)