Generative AI (GenAI) has seen explosive growth in adoption. However, the consumer’s perspective in its use for financial advice is unclear. As with other technologies that are used in processes that involve risk, trust is one of the challenges that need to be overcome. There are personal information privacy concerns as more information is shared, and the ability to process personal information increases.

While the technology has made a breakthrough in its ability to offer financial insight, there are still challenges from the users’ perspective. Firstly there is a wide variety of different financial questions that are asked by the user. A user’s financial questions may be specific such as ‘does stock X usually give a higher dividend than stock Y’, or vague, such as ‘how can my investments make me happier’. Financial decisions often have far reaching, long term implications.

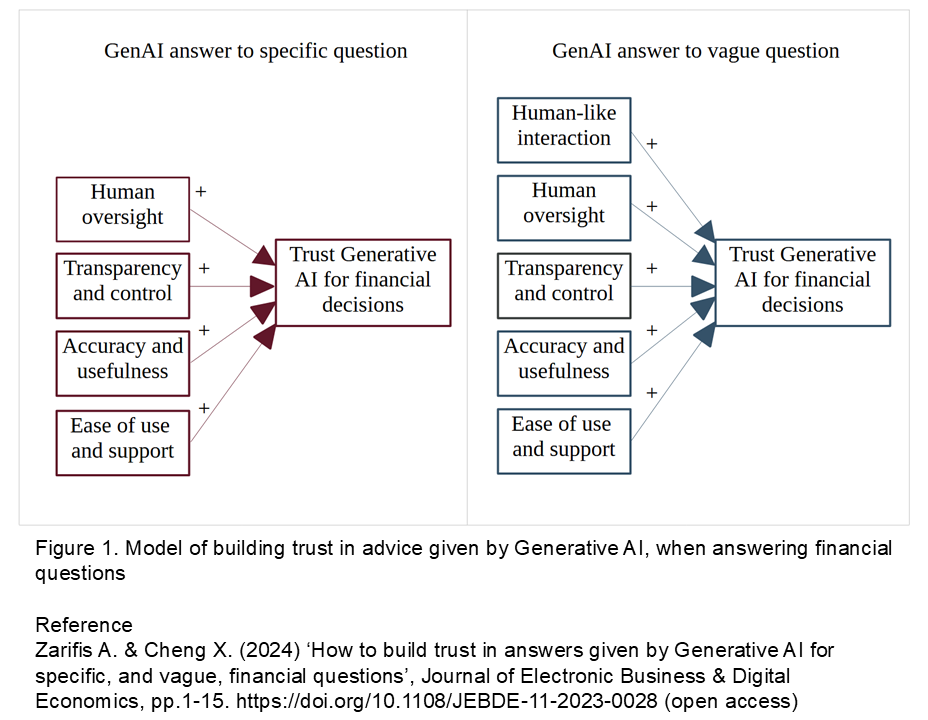

Figure 1. Model of building trust in advise given by Generative AI, when answering financial questions

This research identified four methods to build trust in Generative AI in both of the scenarios, specific and vague financial questions, and one method that only works for vague questions. Humanness has a different effect on trust in the two scenarios. When a question is specific, humanness does not increase trust, while (1) when a question is vague, human-like Generative AI increases trust. The four ways to build trust in both scenarios are: (2) Human oversight and being in the loop, (3) transparency and control, (4) accuracy and usefulness, and finally (5) ease of use and support. For the best results all the methods identified should be used together to build trust. These variables can provide the basis for guidelines to organizations in finance utilizing Generative AI.

A business providing Generative AI for financial decisions must be clear what it is being used for. For example analysing past financial performance to attempt to predict future performance is very different to analysing social media activity. The advise of Generative AI needs to feel like a fully integrated part of the financial community, not just a system. Trust must be built sufficiently to overcome the perceived risk. The findings suggest that the consumer will not follow the ‘pied piper’ blindly, however alluring ‘their song’ of automation and efficiency is.

Reference Zarifis A. & Cheng X. (2024) ‘How to build trust in answers given by Generative AI for specific, and vague, financial questions’, Journal of Electronic Business & Digital Economics, pp.1-15. https://doi.org/10.1108/JEBDE-11-2023-0028 (open access)

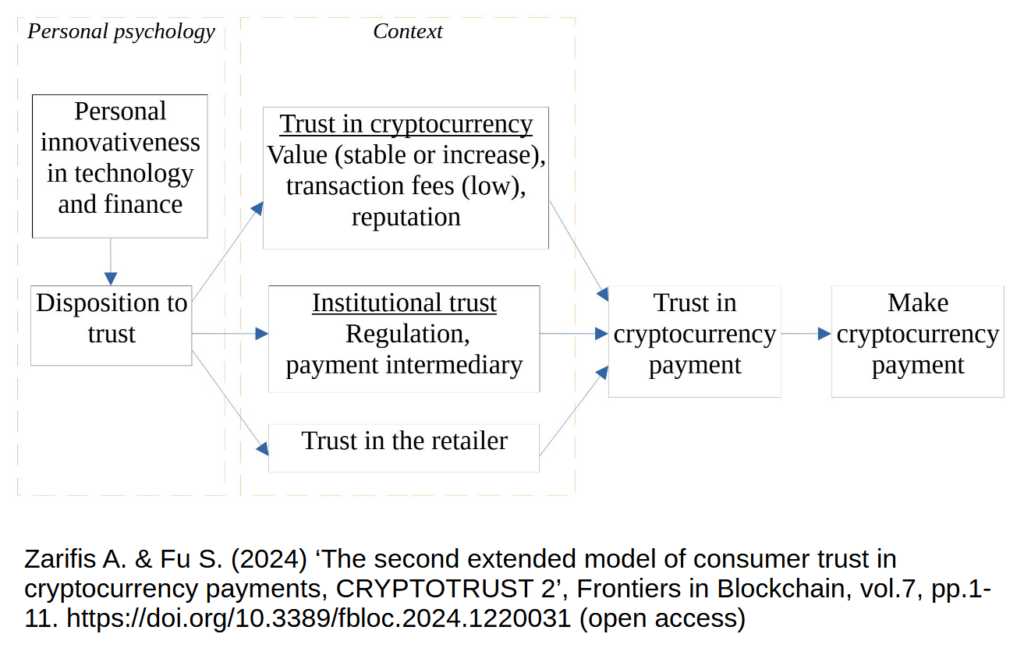

Cryptocurrencies’ popularity is growing despite short-term fluctuations. Peer-reviewed research into trust in cryptocurrency payments started in 2014 (Zarifis et al., 2014, 2015). While the model created then is based on proven theories from psychology, and supported by empirical research, a-lot has changed in the past 10 years. This research re-evaluates and extends the first model of trust in cryptocurrencies and delivers the second extended model of consumer trust in cryptocurrencies CRYPTOTRUST 2 (Zarifis & Fu, 2024) as seen in figure 1.

Figure 1: The second extended model of consumer trust in cryptocurrencies (CRYPTOTRUST 2)

Trust in a cryptocurrency is a multifaceted issue. While some believe that the consumer does not need to trust cryptocurrencies because they utilize blockchain, most people appreciate that you must trust cryptocurrencies, just as you must trust any other technology you use that involves some risk.

The first three variables of the model come from the individual’s psychology: Personal innovativeness is divided into (1) personal innovativeness in technology and (2) personal innovativeness in finance. These two influence (3) personal disposition to trust.

There are then six variables that come from the specific context, and not the person’s psychology: The first three are related to the cryptocurrency itself. These are (4) the stability in the cryptocurrency value, (5) the transaction fees and (6) reputation. Institutional trust is shaped by (7) regulation and (8) payment intermediaries that may be involved in fulfilling the transaction. The last contextual factor is (9) trust in the retailer. The six variables from the context influence (10) trust in the cryptocurrency payment which then, finally, influences (11) the likelihood of making the cryptocurrency payment.

Separating personal innovativeness to personal innovativeness in (1) technology and (2) finance, is a useful distinction as some consumers may have different levels of personal innovativeness for technology and finance. The analysis here supports that these are separate constructs.

This research shows that trust in cryptocurrencies has not changed fundamentally, but it has evolved. All the main actors in the value chain still play a role in building trust. There is more emphasis from the consumer on having a stable value and low transaction fees. This may be because consumers now have more experience with cryptocurrencies, and they are better informed. It may also be because there are more cryptocurrencies available, and other alternatives such as Central Bank Digital Currencies (CBDC), so consumers can review the many alternatives and try to identify the best one.

References

Zarifis A., Cheng X., Dimitriou S. & Efthymiou L. (2015) ‘Trust in digital currency enabled transactions model’, Proceedings of the Mediterranean Conference on Information Systems (MCIS), pp.1-8. https://aisel.aisnet.org/mcis2015/3/

Zarifis A., Efthymiou L., Cheng X. & Demetriou S. (2014) ‘Consumer trust in digital currency enabled transactions’, Lecture Notes in Business Information Processing-Springer, vol.183, pp.241-254. https://doi.org/10.1007/978-3-319-11460-6

Zarifis A. & Fu S. (2024) ‘The second extended model of consumer trust in cryptocurrency payments, CRYPTOTRUST 2’, Frontiers in Blockchain, vol.7, pp.1-11. https://doi.org/10.3389/fbloc.2024.1220031 (open access)

By Dr Alex Zarifis, originally published in The Conversation

I have a confession to make. Despite being an academic, I do not actually read many books. In truth, I don’t often find books about what I like. My interest is on how the latest technologies affect business, and this topic is usually covered better by research articles and the press.

In the days when I was a student and money was tight, I was even less likely to buy books. But one exception was Wikinomics: How Mass Collaboration Changes Everything (2006). Written by Canadian tech thinkers Dan Tapscott and Anthony D. Williams, it captured my interest in how new innovations can change our personal and professional lives – and how exciting this change can be. Clearly I was by no means the only one that felt this way, as the book became a tremendous success.

The title, a compound of Wikipedia pages and economics, followed in the style of the equally successful Freakonomics (2005), but Wikinomics is very much a landmark in its own right. What it conveyed powerfully was that the level of mass collaboration and sharing online was about to move way beyond what we had seen in the first 15 years of the internet, transforming how people did business.

These were much more than mere technological advances, the book argued, and would require a completely different business mindset and philosophy. This was all about openness, sharing, freedom to innovate, and acting globally.

Wikinomics highlights seven new models of collaboration:

1. Open-source software: Software whose source code is made available for everyone to use and build on, which provides a way for firms and coders to coalesce around the same standard. One of the key early driving forces was the Linux operating system, while the book also points to Wikipedia as the archetypal example of the collaborative mindset.

Today, we see many examples of standalone coders coming together from around the world to build applications that are decentralised, meaning they’re not owned by anyone or based anywhere. Decentralised finance (defi), for instance, is offering a new way for people to do everything from trading financial assets to taking out mortgages.

2. Crowdsourcing innovative talent: This allows organisations to solve problems with ideas from outside, typically from other parts of the world. The example given in the book is InnoCentive (now Wazoku Crowd), a site where organisations post scientific challenges and offer rewards for their solution.

3. Prosumers: These are forward-thinking consumers who co-create products and services. In 2006, for instance, users of the virtual world, Second Life, were creating virtual buildings then renting them to other users. Today, fans of computer games such as Total War: Warhammer III are creating new characters and environments in a similar way.

4. Innovators sharing information: Making data widely available for others to use has particular importance in helping solve humanity’s greatest challenges, such as climate change. The increasing popularity of open-access publishing of academic research has been an important step in this direction.

5. Open platforms: Software that allows largely unrestricted access to its content and data gives businesses and individuals more room to collaborate and create new products. One example in the book is Google Maps, which was used by US entrepreneur Paul Rademacher to create a service called HousingMaps. It took data from Craigslist about homes for sale in a given area and pinned them on a map so that anyone searching for a home could see all the available locations at the same time.

Combining capabilities in this way became known as mash-ups, and can be seen today in a service like online bank Revolut. Revolut brings together services and information from a broad variety of organisations and offers them in an integrated way that is easy to use.

6. Mass collaboration in manufacturing: The book noted how a manufacturer like Boeing had shifted from designing everything in-house and sourcing specified parts from individual suppliers to instead having suppliers working together to design parts themselves and then assemble them in teams in Boeing factories.

This switch in emphasis from supply chains to ecosystems has more recently been typified by Shenzhen in China, where collaborative manufacturing in everything from circuits to touchscreens blurs the boundaries between the companies involved.

7. Modern workplaces that avoid hierarchies and silos: Instead of rigid structures, the driving force is social connectivity and fun.

Pros and cons

As is often the case with hugely successful books, Wikinomics was a combination of a great title, good writing and timing. By 2006 many of these trends were well underway. For instance, it was already common for coders to use open-source software like Linux for mass global collaboration. But if the book had been more original, it would not have been so well timed for mass market appeal.

A common criticism of Wikinomics is that it created many obscure terms that will only be familiar to those who have read the book. For example, its fourth collaborative model is called “ideagoras”, which hasn’t exactly caught on. No doubt the authors could have used simpler existing terms, but this is not the main weakness of the book.

With the benefit of hindsight, Wikinomics emphasised the positives of mass collaboration but did a poor job of foreseeing the challenges. Openness has made the world much more vulnerable to cybersecurity hacks, frauds and privacy breaches. Our behaviour online is now endlessly recorded and analysed, making people feel both distrustful and powerless.

What the book did do very well was to frame the issues around the new collaborative economy and explain them clearly. It helped readers to organise the new and old information in their minds, making it easier for them to analyse developments and be part of the revolution.

As a lecturer that teaches business on an executive MBA course to experienced managers, this is something I can appreciate. I cannot always tell them something they have not heard before, but if I can frame the issues well and communicate them clearly, it’s still useful to them. This is ultimately what Wikinomics did: it helped clarify the issues readers already had some understanding of, helping to shape the business zeitgeist for web 2.0.