(chapter 7 in the book)

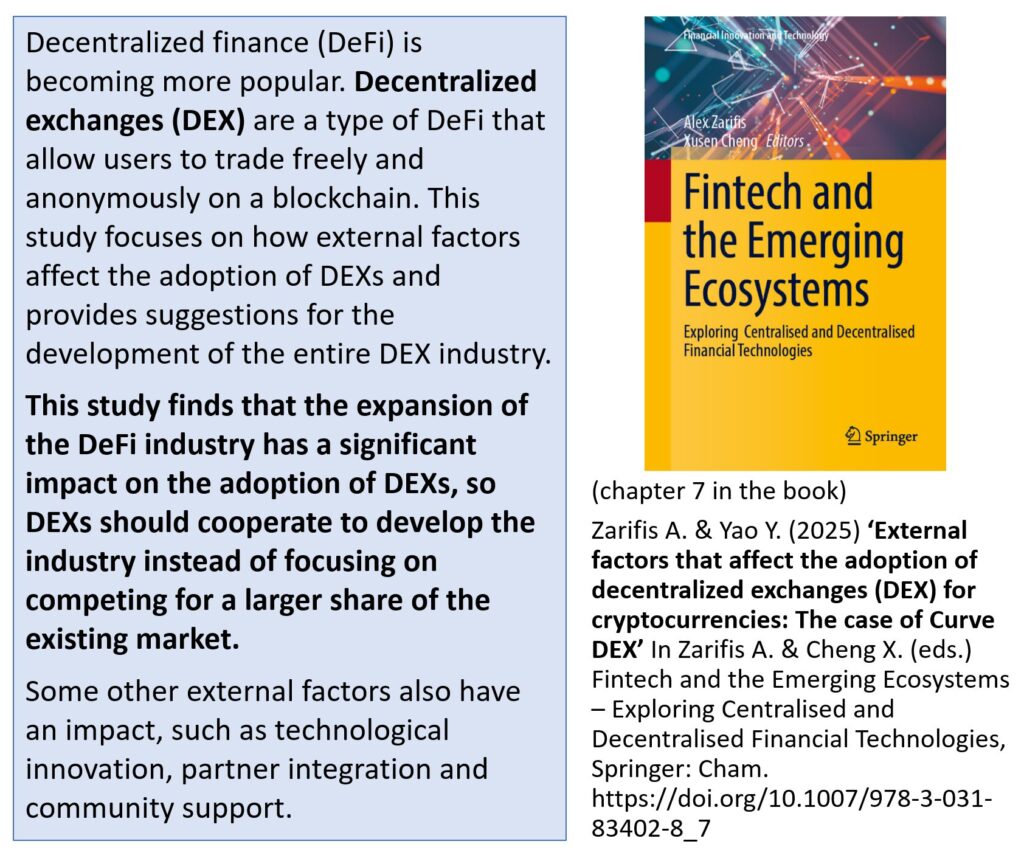

Decentralized finance (DeFi) is becoming more and more popular. Decentralized exchanges (DEX) are a type of DeFi that allow users to trade freely and anonymously on a blockchain.

There are two platforms for cryptocurrency trading, centralized exchange (CEX) and DEX. Most of the exchange volume is happening at CEX because they are easier to use. However, DEXs volume is catching up. The reasons for the popularity of DEXs are linked to the unique advantages of DeFi. First, CEX is a business that requires Know Your Customer (KYC). It requires customers’ identification for registration to comply with anti-money laundering regulations and any other laws from the countries its customers come from. Because of this, users are still concerned about several issues such as privacy and the risk of their wealth being confiscated.

This study focuses on how external factors affect the adoption of DEXs and provides suggestions for the development of the entire DEX industry. The study finds that the expansion of the DeFi industry has a significant impact on the adoption of DEXs, so DEXs should cooperate to develop the industry instead of focusing on competing for a larger share of the existing market. Some other external factors also have an impact, such as technological innovation, partner integration and community support. As DeFi is closely related to the adoption of DEX, the study also discusses the external factors that may affect the adoption of DeFi, namely trust, infrastructure, and regulation.

Figure 1. The factors that affect the adoption of Decentralised Exchanges DEX

Related research is mainly focused on the difference between DEXs, and tries to find how a DEX can gain an advantage over other DEXs, but this research concentrates on the external factors to show how to encourage DEX adoption. While market fluctuations may attract short-term attention and reactions, the long-term development of DEX relies on a stable user base in DeFi and continued expansion of the industry.

This research enriches the theoretical framework of DeFi and sheds light on the relationship between DeFi and DEX. A DEX relies on the liquidity of DeFi, with higher liquidity on the blockchain, the DEX liquidity is expected to be higher, leading to slippage, which means the loss that users suffer when trading on DEX, is reduced. This research provides new insights into understanding the liquidity dynamics of DEXs, extending existing theory on the interplay between liquidity and transaction costs.

References

Zarifis A. & Yao Y. (2025) ‘External factors that affect the adoption of decentralized exchanges (DEX) for cryptocurrencies: The case of Curve DEX’ In Zarifis A. & Cheng X. (eds.) Fintech and the Emerging Ecosystems – Exploring Centralised and Decentralised Financial Technologies, Springer: Cham. https://doi.org/10.1007/978-3-031-83402-8_7