This research is on the state of central bank digital currencies (CBDC) in Latin America. This is the sixth chapter in my report with the University of Cambridge (Proskalovich et al. 2023). I have given a general overview of this report already, so I am just focusing on the chapter on CBDC adoption here.

A CBDC is essentially digital money, issued by a central bank. Unlike most cryptocurrencies that are decentralised, this currency is centralised. This is an important characteristic of the technology that has many implications. For example the central bank may be able to see all the user transactions.

CBDCs can be either wholesale and retail. The general public can use the retail version, while the wholesale version can move large amounts of money between banks. Our research findings suggest that Latin American central banks are focusing mainly on the retail version.

Retail CBDCs can operate with one tier or two tiers. A central bank can issue a one-tier retail digital currency directly to individuals. For the two-tier form, it issues the digital currency to a commercial bank who then offers them to individuals. Most existing implementations in Latin America are hybrid, offering both the one-tier and two-tier forms in parallel. In the hybrid scenario, the user has both a central bank digital wallet, and a retail bank digital wallet.

Figure 1: The motivations behind CBDC adoption in Latin America

These initiatives in Latin America are not completely new. There has been effort to develop and implement them for some time. The first initiative to explore CBDCs was actually back in 2014 in Ecuador. Most countries in Latin America have expressed interest in CBDCs, however, the extent of the engagement varies greatly from (1) exploring the opportunity, to (2) having concluded a pilot project, or (3) launched and available to the public.

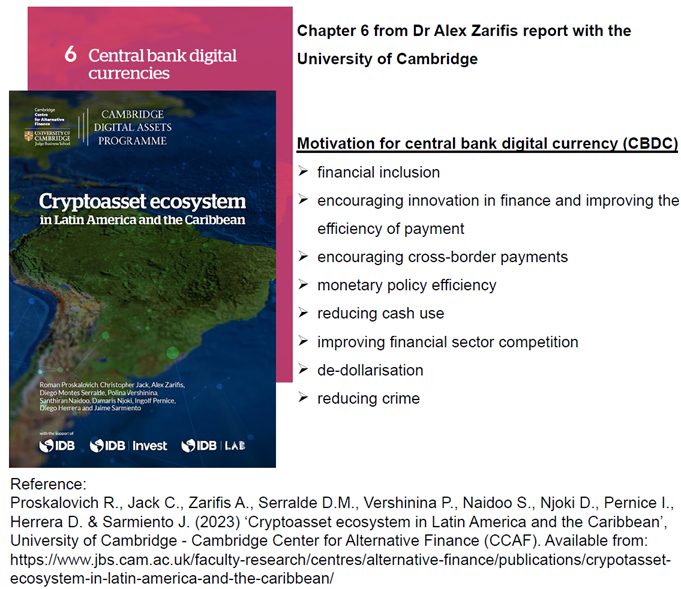

There are several motivation behind creating this form of currency. The two main drivers are usually (1) financial inclusion, and (2) encouraging innovation in finance and improving the efficiency of payments. Other popular reasons are encouraging cross-border payments, monetary policy efficiency, reducing cash use, improving financial sector competition, de-dollarisation and reducing crime.

Challenges include (1) a large informal economy and the popularity of cash, (2) limited financial and digital knowledge, (3) lack of identity documents, (4) limited accessibility, (5) power outages and natural disasters, and (6) currency substitution and capital flight. Capital flight happens for several reasons including high inflation and unfavourable economic conditions.

If you want to learn more about this important part of the cryptoasset ecosystem, you can read the third chapter of the report.

Reference

Proskalovich R., Jack C., Zarifis A., Serralde D.M., Vershinina P., Naidoo S., Njoki D., Pernice I., Herrera D. & Sarmiento J. (2023) ‘Cryptoasset ecosystem in Latin America and the Caribbean’, University of Cambridge – Cambridge Center for Alternative Finance (CCAF). Available from: https://www.jbs.cam.ac.uk/faculty-research/centres/alternative-finance/publications/crypotasset-ecosystem-in-latin-america-and-the-caribbean/